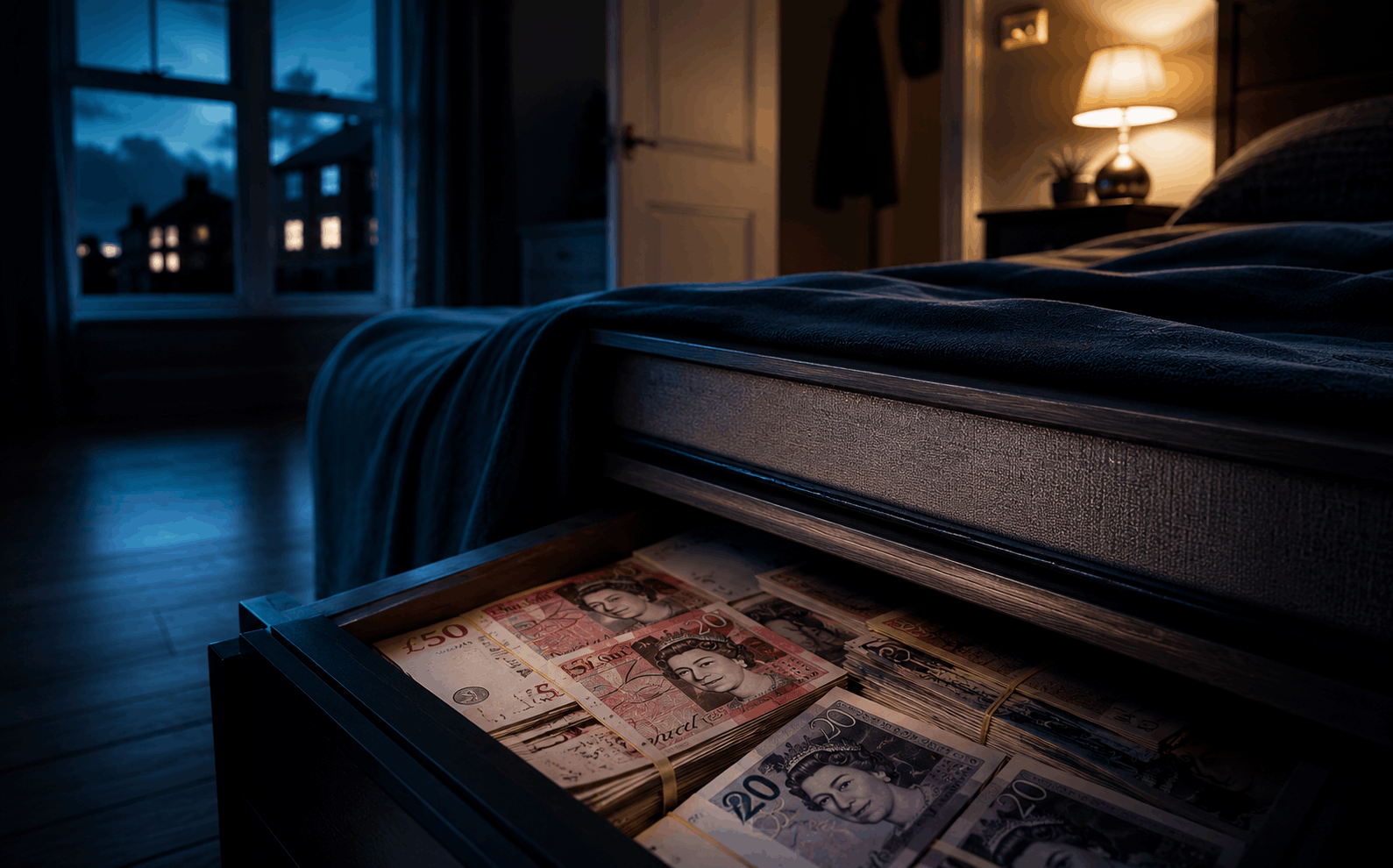

More UK households keep cash at home than banks would like to admit

There's a persistent assumption in financial media that only the paranoid or the elderly keep physical cash at home. That's not accurate. A 2023 survey by the Cash Census found that roughly one in three UK adults keeps "meaningful" amounts of cash at home — and that number barely shifted through the pandemic years.

People do it for understandable reasons: fear of bank failure, distrust of digital systems, emergency preparedness, or simply because it feels tangible and controllable. There's nothing inherently foolish about that instinct. Cash is, after all, still legal tender and carries no counterparty risk.

But the risks are real — and several of them are badly misunderstood, particularly around what home insurance actually covers. This Tips unpacks all of it.

Four risks that every UK household should understand

None of these are reasons to panic — but all of them are reasons to be informed before deciding how much cash to keep at home, and where.

Inflation Erosion

Physical cash earns nothing. At 4% annual inflation, £5,000 in a drawer loses roughly £200 of purchasing power every year — silently and without any warning. Over a decade, you've effectively thrown away more than £2,000 without spending a penny.

Theft & Burglary

Cash is uniquely attractive to burglars because it's untraceable and instantly spendable. Unlike electronics, stolen cash can never be recovered. And if you've exceeded your insurance cash limit — which many people do without realising — your insurer may refuse part or all of the claim.

Fire & Flood Damage

Cash doesn't survive fire or serious water damage. Bank of England notes can be replaced through their Mutilated Notes scheme, but only if you can present enough of the note to prove it existed. Ash and saturated paper rarely meet that threshold. Home safes provide some protection — but not all are fire-rated, and flood damage is a separate issue.

Legal & Tax Scrutiny

There is no legal limit on how much cash you can keep at home in the UK. But holding large, unexplained cash sums can attract attention — from HMRC (particularly if you're self-employed), from lenders assessing mortgage applications, and in theory from law enforcement under the Proceeds of Crime Act 2002. This is rarely a practical risk for ordinary households, but worth knowing if you're holding more than a few thousand pounds.

The numbers that actually matter

Raw statistics only tell part of the story, but these figures help frame the conversation around UK household cash storage honestly.

Cash in circulation in the UK

Despite the rise of digital payments, the value of Bank of England notes in circulation hit record levels post-pandemic. Much of this sits in homes, not tills.

Domestic burglaries per year

England and Wales see roughly 300,000–350,000 recorded domestic burglaries annually. Cash is among the most stolen categories of property — and the least recoverable.

Standard home insurance cash limit

Most standard contents policies cap cash payouts at £1,000–£2,000. Some budget policies apply sub-limits as low as £200. Very few people have read the fine print on this.

FSCS bank deposit protection

The Financial Services Compensation Scheme protects up to £85,000 per person per authorised institution. This is the primary argument against keeping large sums in cash at home.

Average time a burglar spends inside

UK police data suggests most residential burglars spend under 10 minutes inside. They head straight for master bedrooms and obvious hiding spots — bedside tables, wardrobes, under mattresses.

What UK law actually says about cash at home

There is no law in England, Scotland, or Wales that prohibits keeping any amount of cash at home. HMRC cannot raid your property simply because you have large amounts of physical currency, and there is no reporting requirement for domestic cash holdings.

The Proceeds of Crime Act — what it actually means for ordinary people

POCA 2002 is sometimes cited as a reason to fear keeping large sums at home. In practice, this law targets the criminal proceeds of serious organised crime. For a law-abiding citizen, the practical risk is extremely low. However, if cash is seized during an unrelated police investigation, you may be asked to demonstrate its legitimate origin. This is why some financial advisers suggest keeping brief documentation of where significant cash came from — particularly for inheritance, sale of assets, or self-employment income.

Editorial note: We've reviewed HMRC guidance and Law Society briefings. There is no "safe" legal threshold below which you can keep cash at home without documentation — but in practice, households holding amounts equivalent to a few months' salary for genuine emergency use face negligible legal risk. The concern is proportional to the amount involved.

The Bank of England's Mutilated Notes policy

If your cash is damaged by fire, flood, or rodents, you can apply to the Bank of England's mutilated notes team for a replacement. However, the process is selective: you must demonstrate that the notes in question are genuine Bank of England notes and present enough of the physical note to confirm its value. Ash and pulped paper are almost never accepted. Notes damaged by immersion in water have a slightly better chance — but still need to remain legible.

- Claims are assessed case-by-case — there's no guarantee of reimbursement

- Scottish and Northern Irish banknotes are handled by their respective issuing banks

- The process can take several months for larger claims

- Fraudulent claims are taken extremely seriously

What happens during a house move or probate?

Large amounts of undeclared cash can complicate both estate probate and property transactions. Conveyancing solicitors are required by law to report suspicious cash transactions. If you've received a significant inheritance in cash form, documenting it carefully — in writing, with dates — is advisable not for legal protection but for practical convenience.

Self-employed individuals have additional exposure

If you're self-employed and receive cash payments from clients, HMRC is more likely to be interested in large home cash holdings — not because there's anything inherently wrong with it, but because undeclared cash income is a known area of tax avoidance. Good record-keeping is your protection here, not any specific legal limit.

Cash at home vs bank vs digital: an honest comparison

No single option is right for everyone. The best approach for most households is a combination — some liquid cash for genuine emergencies, the rest earning returns elsewhere.

| Factor | Cash at Home | Bank Account | Cash ISA / Savings | Premium Bonds |

|---|---|---|---|---|

| Instant access | Immediate | Same day | 1–90 days | ~3 working days |

| Interest / returns | None | 0.1%–5.2% | 3%–5.5% | ~4.4% tax-free prize rate |

| Protection against inflation | None — loses value | Partial | Strong (if rate > CPI) | Often beats CPI |

| Insurance / FSCS protection | Policy limit only | £85k per institution | £85k FSCS | 100% backed by HM Treasury |

| Theft / loss risk | High — untraceable | Very low | Very low | Negligible |

| Fire / flood risk | Total loss likely | Unaffected | Unaffected | Unaffected |

| Privacy | High | Reported to HMRC | Reported to HMRC | Government-held |

| Tax on returns | N/A | Above PSA allowance | Tax-free (ISA) | Tax-free prizes |

Rates and limits correct as of April 2026. Always verify current terms with your bank or NS&I directly.

Why people keep cash at home — and it's not all irrational

Financial psychology plays a bigger role here than most banks would admit. Many of the reasons people hold physical cash are understandable responses to real uncertainties.

Emergency preparedness

ATM outages, card system failures, and regional power cuts are rare but not imaginary. Keeping a few hundred pounds in cash is genuinely sensible preparation — similar to having a basic first aid kit. The government's own emergency preparedness guidance mentions physical cash as part of household readiness.

Distrust of digital systems

High-profile bank IT failures — Metro Bank, TSB's 2018 meltdown, various NatWest outages — have left many UK customers genuinely cautious about 100% digital dependency. This isn't paranoia; it's a rational response to documented events. The concern is when that caution extends to keeping sums far beyond any reasonable emergency buffer.

Tangibility and control

There is something psychologically different about physical money. You can see it, count it, and touch it. This sense of control is not irrational — it reduces financial anxiety for many people, particularly those who've experienced past financial difficulties or who grew up in households where cash was the norm.

Inheritance habits

A significant portion of home cash holders in the UK are older adults who grew up in an era when cash was simply how money worked. Habits formed over 40 or 50 years are not easily changed by a banking app. For this demographic, the preference is cultural as much as financial.

Privacy concerns

For some, particularly the self-employed or those who have experienced financial surveillance, keeping a degree of financial activity off the record feels protective. This is a legally complex area but emotionally real for a significant minority. It's worth noting: legal income kept as cash at home is not inherently suspicious.

Post-crisis anxiety

The 2008 financial crisis, followed by the 2020 pandemic, created a generation of UK adults with genuinely shaken confidence in financial institutions. Some responded by increasing home cash holdings significantly. Understanding this context is important — these are not foolish decisions, they're anxiety responses to real events that need to be addressed proportionally.

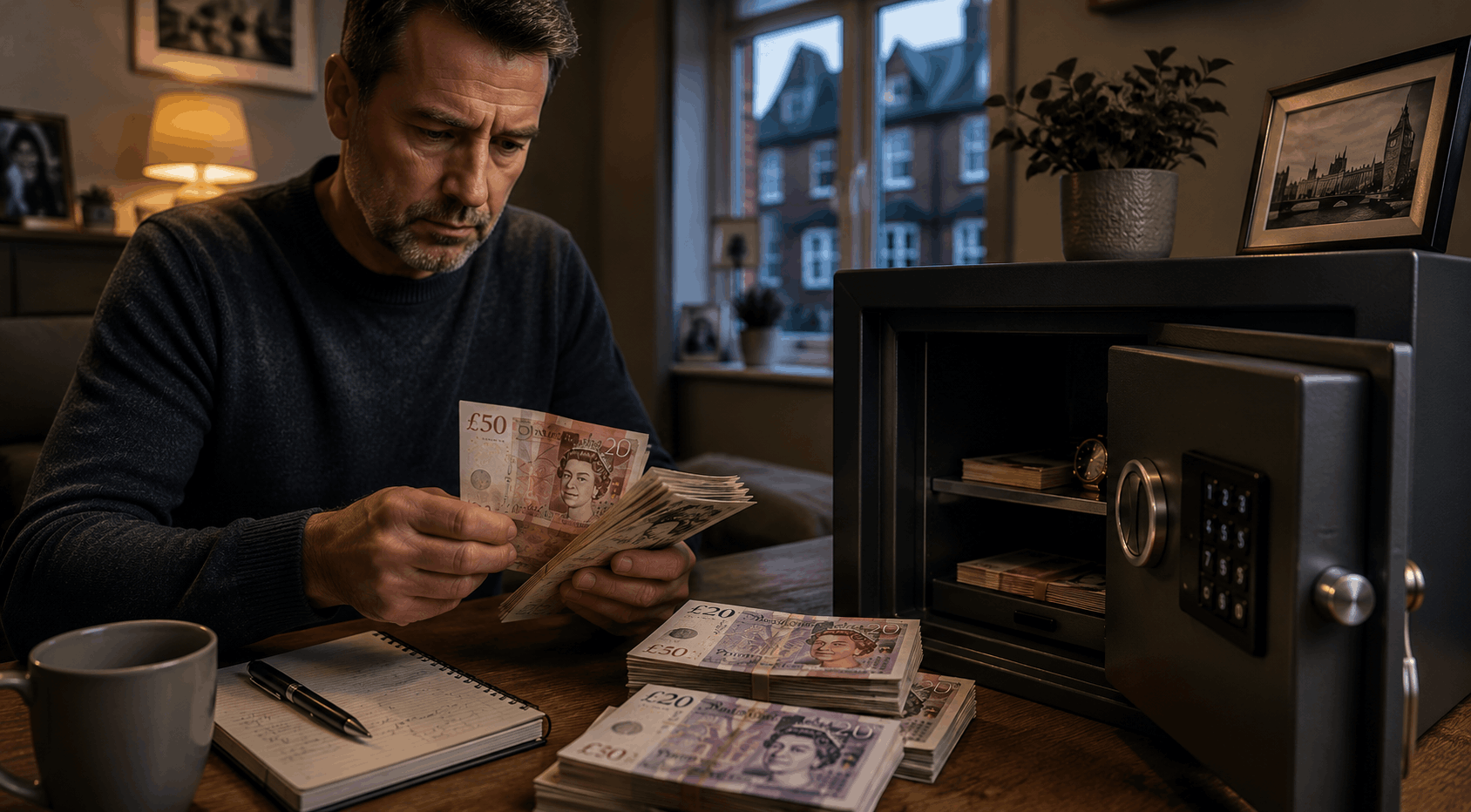

The insurance problem most people ignore

Your home contents policy almost certainly has a cash sub-limit. Most people have never checked what it is. This is one of the most practical things you can verify today.

What home insurance typically covers

Standard UK home contents insurance will usually cover cash as part of your "contents" up to a specified limit — but that limit is almost always much lower than the overall contents sum insured. A policy covering £50,000 of contents might cap cash at £500 or £1,000.

The key term to look for in your policy documents is "money" or "cash." Some policies use the phrase "money as defined below" — which will include things like cheques, postage stamps, and gift cards alongside physical cash.

Watch out: Some budget home insurance policies exclude cash from theft coverage entirely — particularly theft without signs of forced entry. If someone walks in through an unlocked door or window, your cash claim may be declined on this basis.

How safes change the picture

A certified home safe can significantly increase your insurance cash limit — but the rules vary by insurer and by safe grade. Most UK insurers follow the European EN 1143-1 grading system. A Grade 0 safe (the most common consumer model) typically allows insurers to extend cash cover to £6,000. A Grade I safe can raise that to around £10,000.

However — and this is the part many people miss — the safe must usually be bolted to the floor or wall to qualify. A portable safe sitting on a shelf provides almost no meaningful protection against a determined burglar and may not satisfy your policy requirements.

Claims that get rejected

Insurance claims for home cash theft are rejected more often than any other category of contents claim. The most common reasons include: cash exceeding the policy sub-limit; theft without forced entry; cash left accessible rather than in a locked container; and inability to prove the cash existed in the first place.

Practical tip: Keep a photograph of significant cash holdings with a date stamp. A bank withdrawal record, payslip, or receipt showing where the money came from also strengthens any potential claim significantly.

Typical UK cash limits by policy type

These are representative ranges. Individual policies vary significantly. Always read your policy schedule and confirm in writing with your insurer.

Where to keep money that isn't a drawer or a mattress

We're not telling you to hand everything over to a bank. But there are genuine alternatives that address the core concerns around control, access, and security without leaving thousands silently losing value at home.

Easy-access savings account

A well-chosen easy-access savings account from an FSCS-authorised provider gives you same-day or next-day access to funds while earning 4–5% interest. It solves both the inflation problem and the insurance problem simultaneously.

NS&I Premium Bonds

Premium Bonds are backed 100% by HM Treasury — there's no risk of loss on the capital. Prize-equivalent returns run around 4.4% tax-free as of early 2026. You can withdraw funds within a few working days. Not for everyone, but genuinely worth considering for larger amounts.

Certified home safe

If you're going to keep cash at home regardless, a properly installed, insurance-grade safe is the minimum viable option. Look for EN 1143-1 certification, and have it bolted to a concrete floor or solid masonry wall. Budget "fire boxes" sold online typically offer no meaningful security against theft.

Cash ISA

A cash ISA protects your savings from income tax on interest — particularly valuable now that the Personal Savings Allowance has been effectively shrunk for higher-rate taxpayers. Rates are competitive with easy-access accounts, and the tax efficiency compounds over time.

Regular savings accounts

Some high-street banks offer regular savings accounts with rates of 5–8% — but they typically cap monthly deposits at £250–£500 and require you to hold a current account with the same bank. Useful for building a cash reserve gradually, not for parking a lump sum.

Multiple savings providers

If you have more than £85,000 in savings — not as rare as it sounds for people approaching retirement — spreading across multiple FSCS-authorised institutions ensures all of your money is protected. Savings platforms like Raisin make this practical without managing multiple relationships directly.

How to do it properly — if you're going to do it at all

We understand some people will keep cash at home regardless. Here's how to reduce the practical risks as much as possible.

Read your home insurance policy today

Find the "money" or "cash" section in your policy schedule. Make a note of the exact sub-limit and any conditions attached. If you can't find it, call your insurer and get the answer confirmed in writing by email.

Invest in a certified safe — properly installed

EN 1143-1 Grade 0 or above. Bolted to a concrete floor or solid masonry wall. Positioned away from obvious locations. This is the minimum standard that most UK insurers will accept for extended cash cover.

Keep a private written record

Note the approximate amount, where the money came from, and any large-denomination serial numbers. Store this separately from the cash itself — a password manager or encrypted note works well. This helps with insurance claims and provides legal clarity if needed.

Avoid the obvious hiding spots

Burglars in the UK know exactly where people hide cash. Bedroom drawer, bedside table, under the mattress, top shelf of the wardrobe — these are searched within the first two minutes. If you're not using a safe, at least be creative. Better yet: use a safe.

Don't tell people you keep cash at home

This sounds obvious but is frequently overlooked. Cleaners, tradespeople, social media contacts, and even extended family can inadvertently transmit information about home cash holdings. The fewer people who know, the lower your risk profile.

Keep amounts proportionate to actual needs

A genuine emergency cash reserve is sensible. Most financial advisers suggest £200–£500 as a reasonable household emergency float. Holding £5,000 or more at home, uninsured, is almost never justified purely on emergency grounds — and the ongoing inflation cost adds up quickly.

Frequently asked questions

Real questions UK households ask about keeping cash at home — answered plainly.

No. There is no law in England, Scotland, or Wales that sets a limit on how much cash you can keep at home. Physical cash is legal tender and there is no reporting requirement for domestic cash holdings.

The confusion often stems from Proceeds of Crime Act legislation, which gives authorities powers to seize cash believed to be criminal proceeds. But this power applies to criminal investigations — it doesn't mean ordinary households with legitimately obtained savings face any legal risk from keeping cash at home.

Most financial advisers and emergency preparedness guidance suggests keeping £200–£500 as a household emergency cash float. This is enough to cover several days of essential spending if card systems go down, ATMs are unavailable, or you face a short-term income disruption.

Beyond that, the case for keeping physical cash at home (rather than in an accessible savings account) weakens significantly. The inflation cost, security risk, and insurance exposure all increase without proportionate benefit.

Usually yes — but up to a specified limit that is often much lower than you might assume. Standard UK home contents policies typically cap cash at £500–£1,500. Budget comparison-site policies can be as low as £200.

Additionally, many policies require forced entry for a theft claim to succeed. If someone entered through an unlocked door or window — or it was an "inside job" — the claim may be declined. Always read the specific conditions in your policy's money section, and confirm with your insurer in writing if you're unsure.

In most cases, physical cash is destroyed beyond recovery in a serious house fire. The Bank of England operates a Mutilated Notes scheme that can replace damaged notes — but only if enough of the note remains to confirm its authenticity and denomination. Ash rarely qualifies.

A fire-rated safe (rated to keep internal temperatures below 175°C, which is the threshold at which paper chars) provides meaningful protection, but not all home safes marketed as "fire safes" meet this standard. Look for EN 1047-1 classification or an equivalent independently tested fire rating before trusting a safe with cash in a fire scenario.

For most employed people keeping reasonable amounts of cash at home, the practical answer is no. HMRC's focus is on unreported income, not on where people store money they've already paid tax on.

The picture is different if you're self-employed and receive cash payments. In that context, large unexplained home cash holdings could be flagged during an investigation as evidence of unreported income. Good record-keeping — knowing where your cash came from and having documentation to prove it — is the straightforward protection here.

This is a legitimate concern, but the risk is much lower than many people believe. The Financial Services Compensation Scheme (FSCS) guarantees deposits up to £85,000 per person per authorised institution. If your bank fails, you receive that money back — typically within seven working days under current rules.

If you have more than £85,000 in savings, spreading it across multiple FSCS-authorised institutions is the appropriate response — not keeping it in cash at home. The FSCS has never failed to compensate eligible depositors since its creation.

Yes, in several ways. First, a certified home safe (EN 1143-1 Grade 0 or above, properly installed) will usually allow your insurer to extend cash cover to £6,000 or more. Second, some specialist insurers offer high-value home contents policies with negotiated cash limits. Third, you can sometimes add a specific "money extension" to an existing policy for an additional premium.

Always get any coverage extensions confirmed in writing and check whether there are conditions attached — such as the safe being bolted to a structural wall or floor.

For a few hundred pounds, a certified safe is probably not worth the cost (typically £150–£500 for a decent Grade 0 model, plus installation). The insurance benefits kick in at higher amounts, and the security improvement for small sums is marginal.

However, if you regularly keep over £1,000 at home — or store important documents, passports, or jewellery — the investment makes more sense. The safe's value isn't purely for cash; it protects anything irreplaceable stored inside it.

Get the StableHouse UK Cash Storage Checklist

A one-page PDF summary of everything on this page — including the insurance limit reference table, safe grades explained, and the emergency cash checklist. No spam, no ongoing emails.

We send one email only. See our privacy policy.